December 26, 2025:

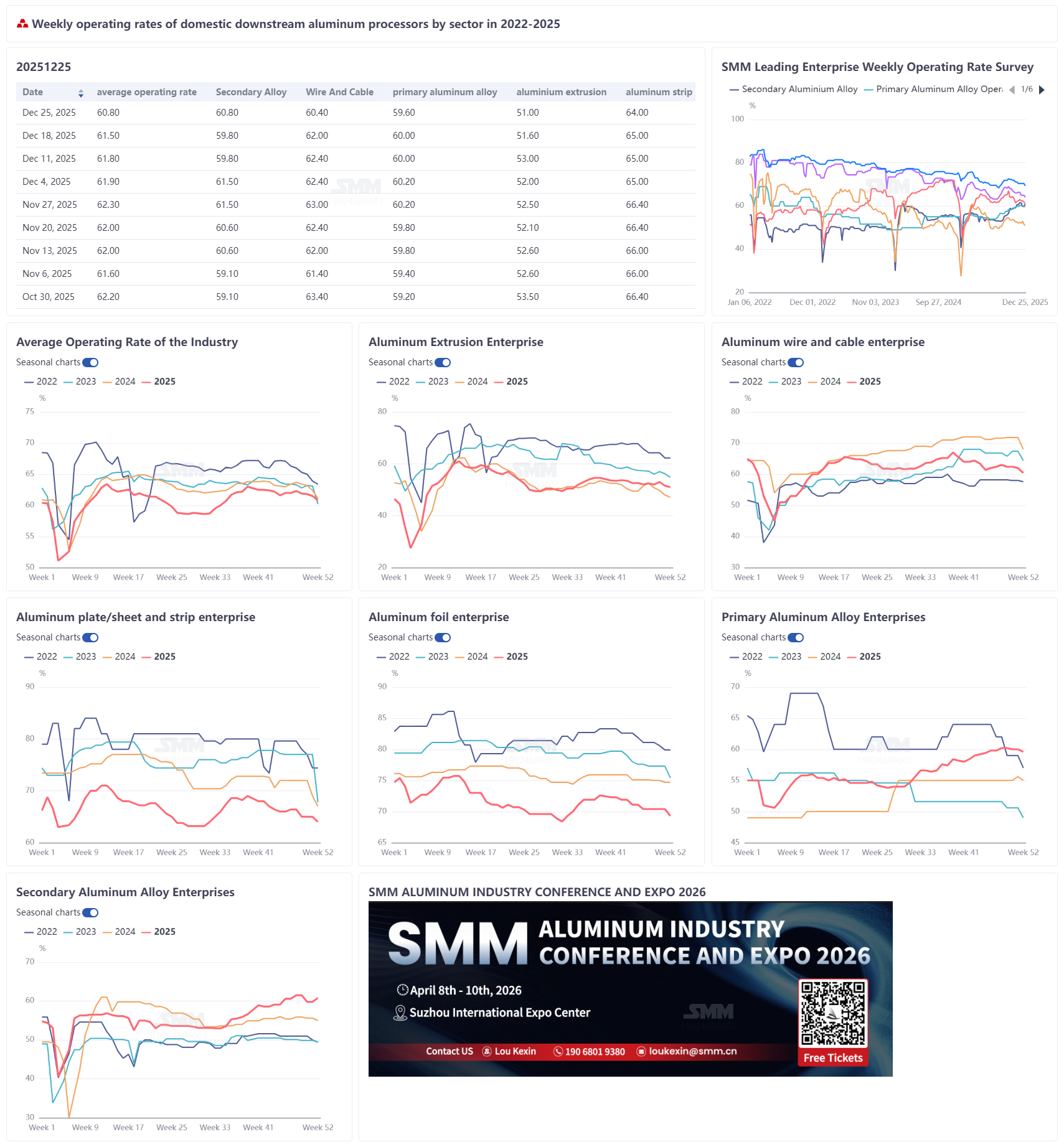

The weekly operating rate of leading domestic aluminum downstream processing enterprises fell 0.6 percentage points WoW to 60.8%. Due to weak orders, environmental protection-related controls, and high aluminum prices, downstream operations further deepened into the off-season. By sector, the operating rate of primary aluminum alloy pulled back 0.4 percentage points to 59.6%. Long-term contract deliveries at mainstream enterprises remained stable, but persistently high aluminum prices continued to suppress spot order transactions, with downstream purchase willingness remaining sluggish. The operating rate of aluminum wire and cable declined 0.6 percentage points to 60.6%, as environmental protection-related controls in Henan affected enterprise operating capacity, and power grid order matching progressed slowly, keeping operations weak. The operating rate of aluminum extrusion edged down 0.6 percentage points to 51.0%. Construction profiles remained sluggish due to slowed winter construction and payment collection pressures, while reduced PV production schedules dragged on industrial profiles; only automotive and ESS profiles remained basically stable. The operating rate of aluminum plate/sheet and strip dropped 1.0 percentage point to 64.0%, as intensified environmental protection-driven production restrictions in Henan, combined with high aluminum price suppression, led to a significant decline in construction and packaging orders, and expectations of can stock processing fee increases failed to alter the weak pattern. The operating rate of aluminum foil decreased 1.1 percentage points MoM to 69.3%, with traditional air-conditioner foil and decorative foil demand weakening, while single-zero packaging foil was supported by year-end stockpiling; new energy products like battery foil saw limited incremental growth. The operating rate of secondary aluminum producers rebounded 1.0 percentage point to 60.8%, mainly driven by the lifting of environmental protection-related controls in Chongqing, but small and medium-sized producers were constrained by high aluminum scrap costs and pressure from die-casting plant production cuts, limiting capacity release. SMM expects industry operating rates to continue weak consolidation in the short term, with further downside room as the consumption off-season deepens, environmental protection constraints remain rigid, and high aluminum prices persist.

Primary Aluminum Alloy: The industry operating rate this week was approximately 59.6%, down 0.4 percentage points WoW, showing a slight downward trend overall. Supply side, long-term contract deliveries remained stable, maintaining the original pace without significant fluctuations. However, spot order transaction volume shrank, leading to a further decline in the overall operating rate. Demand side, market buying sentiment was generally low, primarily because recent aluminum prices remained high, suppressing downstream enterprises' purchase willingness. Most enterprises currently prefer to wait-and-see, generally believing aluminum prices are still in a high range, and thus are not in a hurry to increase purchases of primary aluminum alloy, showing a clear cautious mindset. Overall, the market is expected to continue its current slow downward trend next week, with subsequent changes needing close attention to the impact of aluminum price fluctuations. Aluminum plate/sheet and strip: The operating rate for leading enterprises in the aluminum plate/sheet and strip sector fell 1 percentage point WoW to 64.0%, indicating increasing operational pressure. Environmental protection-driven production restrictions escalated sharply in central China, with Gongyi issuing a red alert for air pollution starting at 12:00 on December 24, expected to last until December 28. Combined with existing environmental protection-related controls in Luoyang and Sanmenxia, production and transportation faced significant constraints, making it difficult for operating conditions to improve before the New Year's Day holiday. Some enterprises, facing continuous order declines, planned to slow down their production pace and conduct concentrated equipment maintenance. On the export front, customs data showed aluminum plate/sheet and strip exports reached 272,100 mt in November, up 13% MoM, indicating a temporary recovery. Looking ahead to next week, with the consumption off-season deepening, rigid environmental constraints and high aluminum price risks coexisting, and coupled with the later timing of the 2026 Chinese New Year holiday, order books lack effective support. The operating rate for aluminum plate/sheet and strip is expected to remain low in the short term, with little chance for substantial improvement.

Aluminum wire and cable: The weekly operating rate for the aluminum wire and cable industry fell further to 60.6% this week, continuing its downward fluctuation. The decline was mainly due to intensified environmental protection-related controls in Gongyi, Henan, which restricted local producers' capacity, coupled with slow progress in matching power grid orders by year-end, resulting in insufficient actual support. From an operational perspective, some producers have turned to exports as a primary order source, but overseas new energy project progress slowed due to the Christmas holiday, putting short-term pressure on export orders. Meanwhile, although power grid tenders advanced, new tender orders have not entered the cargo pick-up cycle, sustaining a pattern of "strong expectations versus weak reality." Concerns among enterprises about next year's goods pick-up pace persist. Looking ahead to next week, with ongoing environmental production restrictions, slow order matching, and weak year-end stockpiling willingness, the aluminum wire and cable operating rate is expected to remain under pressure and continue its decline.

Aluminum extrusion: The domestic aluminum extrusion operating rate pulled back 0.6 percentage points WoW to 51%, primarily due to lower operating rates at some sample enterprises in east and central China. In the architectural extrusion segment, typical year-end off-season characteristics were pronounced. On one hand, lower temperatures led to work stoppages and production cuts at construction projects; on the other, rising pressure for year-end payments made downstream customers more cautious in their purchasing decisions. Consequently, enterprises in Shandong, Zhejiang, and Hunan experienced varying degrees of decline in their operating rates. Among them, large and medium-sized enterprises maintained relatively stable operating rates by compensating for reduced architectural extrusion orders with industrial extrusion business, whereas small enterprises showed relatively sluggish performance. For industrial extrusions, overall performance, though better than architectural extrusions, was constrained by high aluminum prices, leading downstream purchases to focus on rigid demand and orders to become smaller in size, keeping extrusion enterprises' operating costs high. Additionally, some enterprises in Shandong reported that orders related to the power sector involved long payment cycles, resulting in high capital costs and generally weak expectations for future operating rates. Overall, the aluminum extrusion industry is currently in an off-season cycle, lacking upward drivers for its operating rate, which is expected to remain in the doldrums in the short term. Aluminum foil: This week, the operating rate of leading aluminum foil enterprises dropped 1.1 percentage points MoM to 69.3%. In terms of order structure, traditional consumption sectors showed significant weakness. Entering late December, order fulfillment for new energy-related products such as battery foil and brazing sheet was relatively high, leading to adjustments in the production pace. On the export side, customs data showed aluminum foil exports in November reached 109,800 mt, up 4% MoM, primarily boosted by overseas stockpiling demand ahead of Thanksgiving and Christmas. In the short term, the weakness in traditional consumption sectors is hard to reverse, risks of high aluminum prices persist, and order support remains insufficient. Coupled with the delayed stockpiling period for the 2026 Chinese New Year shifting to mid-January, the industry overall lacks strong growth drivers in demand. The operating rate in the aluminum foil sector is expected to fluctuate rangebound.

Secondary aluminum: This week, the operating rate of leading secondary aluminum enterprises rebounded 1.0 percentage point MoM to 60.8%, mainly benefiting from the lifting of environmental protection-related controls in Chongqing, where the operating rate of sampled local enterprises has returned to normal levels. However, regions such as Henan and Hebei still face impacts from fluctuations in environmental protection policy, continuously restricting capacity release. Cost side, driven by stronger aluminum prices and record-high copper prices, aluminum scrap prices (especially aluminum tense scrap) rose rapidly and showed strong resistance to declines even during aluminum price pullbacks, keeping production costs for secondary aluminum enterprises high. Currently, some enterprises saw dampened production enthusiasm due to tight aluminum scrap supply and losses, leading to a slight drop in overall industry production. Combined with prices fluctuating at highs and seasonal off-season demand, downstream purchase willingness weakened, and demand-side support for the operating rate was insufficient. Considering the approaching New Year holiday, the operating rate of secondary aluminum enterprises is expected to drop back slightly next week.